Health & Fitness

Controversy Follows Employment Report – Stocks Near 5 Year Highs.

In this week's column we update you on this weeks market activity and take closer look at the controversial Friday jobs reports. See how this affects you.

USA Markets Close Near Five Year Highs

It was another good week for the stock markets on a global basis. The markets moved higher in response to some surprisingly strong economic reports that were released this week. The S&P 500 gained 1.5% and closed on Friday near it highs for the week at 1,461.

Find out what's happening in Redmondwith free, real-time updates from Patch.

The S&P 500 is now 6 points away from establishing a new 5 year high. With just 11 weeks remaining in 2012, the S&P 500 is currently on pace for it’s best year since 2009. If the S&P 500 can clear the 1,466 level next week then it is probable that there would be another surge higher on technical buying of the new 5 year highs.

In The Photo Section is a chart of the S&P 500 for 2012 that illustrates the road that the USA markets have traveled this year in order to reach their 16% year to date gains:

Find out what's happening in Redmondwith free, real-time updates from Patch.

(See Image of Chart of the S&P 500 in The Photo Section)

Earnings season starts next week. Between earnings season and the upcoming election we expect more volatility in the markets. We expect that earnings for most companies will be somewhat disappointing. However, expectations for the 3rd quarter earnings are very low now. If companies can exceed the low levels of expectations then the foundation for another move higher and new five year highs is in place.

We will have a clearer picture of the health of the US economy and business conditions three weeks from now after a majority of USA companies have reported their results.

Economic Reports Show Surprising Strength

The near term outlook for the economy grew brighter this week as most economic reports such as Auto Sales, Manufacturing and Factory Orders reported results that were stronger than what had been expected. Two reports in particular provided both a boost of optimism to the stock markets at the beginning of the week and some controversy to the political landscape at the end of the week. They are:

- The Institute of Supply Management (ISM) Non-Manufacturing Index report.

- The September Employment Reports

We present the results of both of these economic indicators reports below.

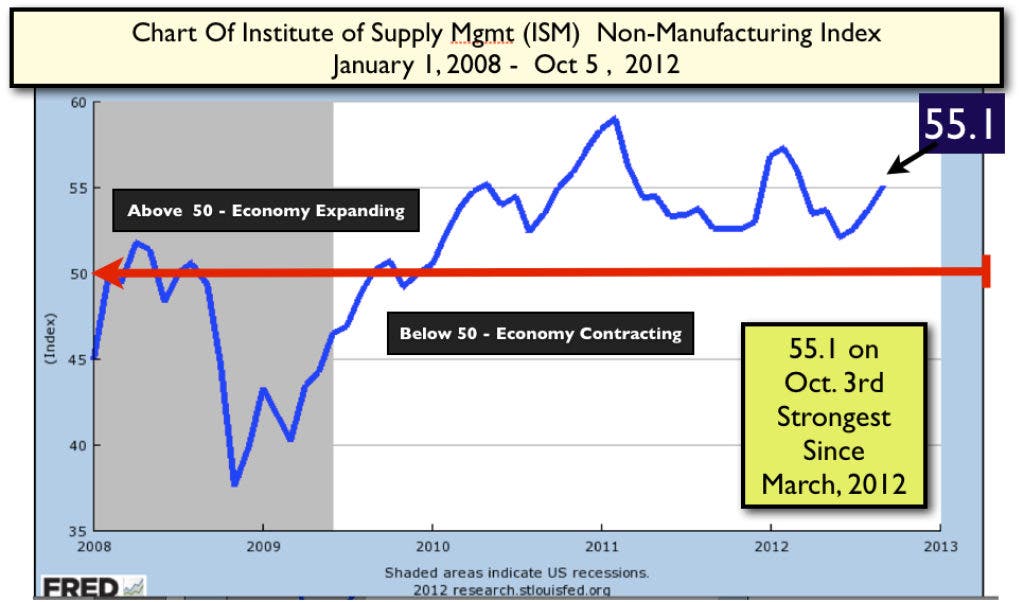

The Institute of Supply Management (ISM) Non-Manufacturing Index is based on monthly surveys sent to hundreds of Purchasing Managers working in the service industries throughout the USA. Each of these Purchasing Managers will report to the Institute the change in purchasing patterns for the current month when compared to the previous month.

The Purchasing Managers activities covers General Business Activity, New Orders, Inventory Changes and employment.

Many economists consider the ISM reports to be the most reliable economic indicator of real time strength or weakness of the overall economy. This Non-Manufacturing Index is most important because it is measuring the Services Sector of the economy which is somewhere near 80% of the entire economy.

On Wednesday October 3rd, the ISM reported that the composite Non-Manufacturing Index for September came in at a healthy 55.1.

In The Photo Section is a 5 year chart of the (ISM) Non-Manufacturing Index. This chart and index is very easy to understand. When the ISM Index is above 50 then the economy is said to be in expansion. When below 50 then the economy is contracting. We show this 50 expansion/contraction line on the chart with a Red Arrow.

(See Image of Chart of ISM Non-Manuafacturing Index in The Photo Section)

Note how low the Non-Manufacturing index fell during the 2008-2009 economic panic.

September Employment Reports Create Controversy

The second economic report(s) we would like to present is the The September Employment Reports. These are actually a series of reports that measure unemployment and job creation. Their release on Friday, October 5th led to claims that the numbers had been manipulated. Here are the results:

- Unemployment Rate 7.8% (expected 8.2%). This is the lowest since 2009.

- Job Growth 114,000 (expected 113,000).

- Labor Force Participation Rate (which is the % of working age adults in the work force) is 63.6%.

Additionally there were more adjustments to the prior months job growth totals – Job growth for July which was originally reported at 141,000 was revised higher to 181,000. August job growth numbers were also adjusted higher – from 96,000 to 142,000.

The immediate reaction to the release of the September Job Reports was disbelief and claims of political maneuvering. Now while we believe that both parties are capable and are guilty of massaging data, we do not think that is the case here in these job reports because of the following:

1. We have reported the on the Recent Strength in the Housing and Home Building Industries and home building activity creates more jobs than any other type of economic activity.

2. Auto Sales for the past few months have been steadily increasing and are near five year highs. There is a near 100% correlation between auto sales growth and employment growth. Auto sales in September were the highest since March, 2008.

3. The Latest Consumer Confidence report also shows people are much more optimistic – which foots with an improving job market – here is the excerpt from the most recent Consumer Confidence report in Italics below:

......The Consumer Confidence Index rebounded in September and is back to levels seen earlier this year (71.6 in February 2012). Consumers were more positive in their assessment of current conditions, in particular the job market, and considerably more optimistic about the short-term outlook for business conditions, employment and their financial situation.....

So while we can agree that governments are constantly massaging statistics that they release to the general public, we think that the other economic reports show support for and provides independent confirmation of an improving labor market that matches the results that was released in the controversial jobs reports on Friday.

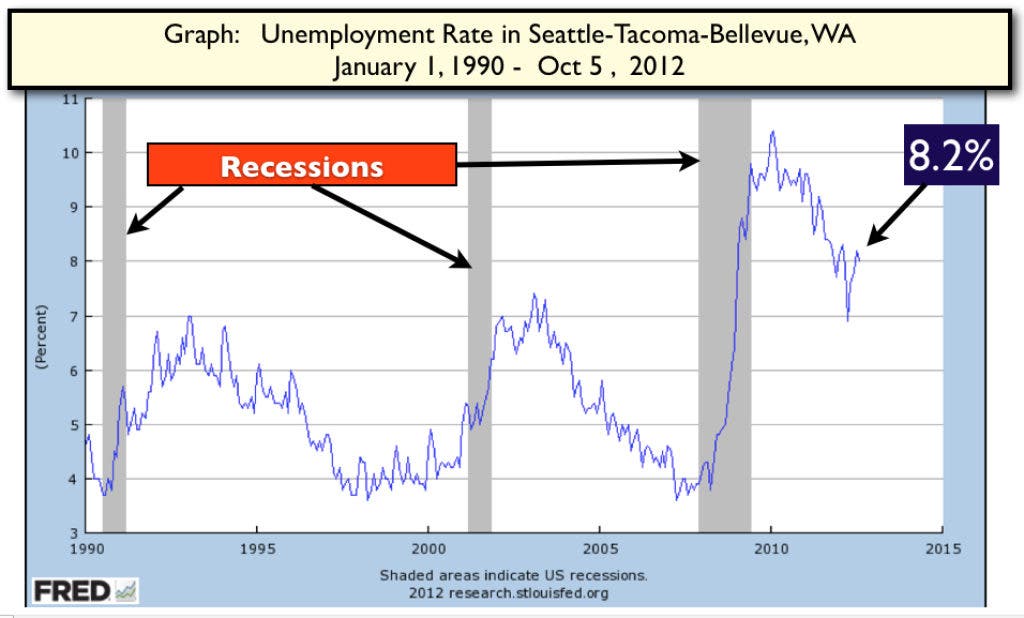

Now to put our own local unemployment condition in it’s historical context, In The Photo Section we present a chart of the Greater Seattle-Bellevue Tacoma unemployment rate for the past 22 years. The grey areas on the chart are recessions. The most recent report of unemployment for the greater Seattle-Bellevue area showed unemployment was at 8.2%.

(See Image of Chart of the Seattle-Bellevue Area Unemployment in The Photo Section)

We would like to note the following. Even though labor market conditions are improving, they are improving from the worse levels of most everyone’s lifetimes. For the many people who are without a job or under-employed now, we are not in a recession, instead we remain firmly in a depression.

It has not been this difficult for people who have had the misfortune of unemployment to find another job for 80 years. Furthermore we have read reports where for the people who have lost their jobs since 2009 but successfully found another one, 92% of these people are making less on their new jobs than they were on the prior job that they lost. And these are the “Lucky Ones” who have found a job.

A pattern has emerged at the end of the last three recessions (1990, 2002, 2009) where with each successive recession, it takes longer and longer for the job markets to return to their pre-recession employment levels. Furthermore, with each successive recession since 1990 we have also seen the elimination of entire sectors of higher paying jobs and replacement of those higher quality jobs with lower paying jobs. So while the unemployment rate has come down after each of the last three recessions, most the new jobs that are replacing the jobs that were lost during the recession are lower paying ones.

This trend shows that the current macro-economic conditions are failing to produce quality, middle class paying jobs in sufficient numbers for the American public.

The American Economic job creation machine has a lot of repairs that needs tending to. The primary issue of this election and all future elections should be a laser focus on policies and programs that promote and support businesses that create quality jobs for people – we think manufacturing would be a good place to start.

Closing Thoughts

The Stock markets continue to work off their overbought conditions. The markets have come a long way since their June 2nd lows. We do not believe that now is a good time to put fresh money to work with stocks near five year highs. There will be the inevitable correction in USA equities in the future and that will be a more opportune time to consider increasing exposure.

We have noted an improving condition and out-performance of stocks and stock markets in emerging market economies. Up until recently the USA markets had been out-performing the emerging markets since November, 2011. We will be monitoring this out-performance by emerging markets closely to see how it develops over the next few weeks for investment opportunities.

---

John Patrick Bray, CPA, is president of Bellevue-based Reliance Investment Management LLC .

This communication reflects the opinions of Reliance Investment Management LLC and is being provided for informational purposes only and is not intended as a recommendation, an offer or solicitation for the purchase or sale of any security referenced herein or investment advice. It is being provided to you on the condition that it will not form the primary basis for any investment decision. We recommend that you consult with your investment advisor before the purchase or sale of any securities. The information contained herein is of the date referenced and Reliance Investment Management LLC does not undertake an obligation to update such information. Reliance Investment Management LLC has obtained all market prices, data and other information from sources believed to be reliable although its accuracy or completeness cannot be guaranteed. Such information is subject to change without notice. The securities mentioned herein may not be suitable for all investors.